“Tomorrow belongs to those who can hear it coming.”

-DAVID BOWIE

When a choice isn’t a choice. For this month’s edition of our Guest EVA, we are again showcasing one of the financial world’s rising-star newsletter writers, Ben Hunt. In addition to being the developer of the Epsilon Theory website, Ben has become increasingly known for coining the phrases “The Golden Age of the Central Banker” and “The Era of Central Bank Omnipotence”. Both of these expressions relate to his belief that we are in an era where markets are almost totally reliant on the machinations of the Fed and its developed world peers (a view Evergreen shares).

Recently, he has downgraded his first characterization to the “The Silver Age of the Central Banker” due to some fraying around the edges of their alleged superpowers. It’s important to convey right up front that Ben’s take on this isn’t bullish or bearish. It just acknowledges the reality of the environment the Fed and its counterparts have created. In fact, toward the end of his article, Ben brings up a new central bank tool that has significant positive implications for supporting asset prices, a development we will elaborate on shortly.

You will soon see that this piece was written for investment professionals. Nevertheless, it contains valuable insights for all investors seeking to cope with an interest rate paradigm never witnessed before in human history. Because these are truly uncharted waters, the crystal balls of even investment professionals are unusually cloudy (emphasis on “unusually”). Thus, as Ben writes, relying on standard portfolio design tactics is unlikely to produce acceptable returns. In his view, this forces investors to face a “Hobson’s Choice” between being satisfied with earning almost nothing or adopting an unconventional position.

The latter, of course, is, as always, fraught with copious amounts of reputational, career, and psychological risks. As Ben notes, John Maynard Keynes summed this up well when he said, some eighty years ago, “It is better for your reputation to fail conventionally than to succeed unconventionally.” As a firm that has continually railed against the serial bubbles since 2002 (and, personally, as far back as the late 1980s), we know well the challenges of resisting group-think in striving to succeed unconventionally.

Ben believes that the era of central bank omnipotence won’t come to an end until someone like European Central Bank (ECB) chief Mario Draghi announces to the world: “Well, there’s really nothing more we can do…sorry…” (Or, perhaps, “scusi”). However, Super Mario, as he’s known, is still flexing his monetary muscles. In March, he took the momentous step of committing the ECB to buying corporate bonds for the first time ever (naturally, using out-of-thin-air money).

This is where it gets interesting—and potentially bullish—for US income investors. Because the ECB is willing to acquire corporate debt issued in Europe by US companies that have operations on the Continent, nearly all of our multinational (i.e., blue chip) enterprises can access this program. Several have already taken advantage of the lower yields that have resulted from the announcement, even though the ECB’s buying binge doesn’t start until next month. For example, McDonald’s recently issued a five-year euro-denominated bond at an interest rate of just 0.45%!

Consequently, this program will have the effect of lowering credit spreads (the gap between government and corporate bond yields), at least for those companies that can access it. As we have noted so many times in these pages, credit spreads exert a tremendous influence on financial markets. This should mean that spreads won’t widen out as much as they would without the ECB’s ravenous appetite for bond-buying. And that will be very good news for US companies during the next market seizure, such as we saw earlier this year when spreads approached recession-type levels. (The Fed might want to imitate the ECB but may be restricted from doing so by its charter; we wouldn’t discount the possibility it will try to amend, or get around, any prohibitions, however.)

Tighter credit spreads should also be a notable boon to those investment areas that Ben is suggesting (and Evergreen is heavily involved with) such as MLPs (pipelines and other energy infrastructure) and Canadian real estate investment trusts. In other words, real assets that generate real cash flow.

He further believes an investor needs to be willing to put his or her money to work anywhere in the capital structure. This may mean buying a company’s bonds when they look more attractive than its stock. (In this regard, Evergreen recently bought an investment grade bond yielding nearly 9%, believing it more appealing from a risk/reward standpoint than its underlying equity).

Like us, he is also partial to gold as protection for when the golden era of central bankers doesn’t just devolve to silver but all the way to lead. The odds of that happening, good reader, are virtually a lead-pipe cinch.

DAVID HAY

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

(Note: This is an abridged version of Ben’s March 16th, 2016, “Hobson’s Choice” letter. To access the full issue, please click on this link.)

By Ben Hunt

The Hobson’s Choice that nearly every investor, allocator, or financial advisor faces today is always some variation of the famous quote from John Maynard Keynes: it’s better for your reputation (i.e., your business) to fail conventionally than to succeed unconventionally. Every investment professional I’ve ever met – every. single. one. – wrestles with this dilemma. So do I. We’ve all seen examples in our portfolio results that the conventional tools aren’t working. We know that the words we hear from our Dear Leaders and the articles we read from our Papers of Record are designed to manipulate and entertain us, not inform us. We want to succeed, and we feel in our gut that we should be trying something new and (maybe) better. But not if it means losing our clients or losing the support of our Board or losing the support of that little voice of convention inside each of our heads. It’s that last bit that’s probably the most powerful. As George Orwell so correctly observed about human psychology, the most terrifying part of hearing Big Brother say that two plus two equals five isn’t that they might kill you for believing otherwise, but that you think they might be right!

And make no mistake about it, our Hobson’s Choice is getting worse. Investing according to conventional wisdom has always been the reputationally safe decision, but in the policy-controlled markets to come, investing according to conventional wisdom may well be the only legally safe decision.

So here’s what I’m not going to do. I’m not going to discuss “alternative strategies” that are always set off to the side in a little section of their own on an investment menu, intentionally organized and presented as if to say “Careful now! Here are some exotic side dishes that you might use to spice up your core portfolio a bit, but you’d be crazy to make a meal out of this … not that we’d let you do that anyway.” I’m not going to perpetuate the Hobson’s Choice game and its charade of false choices and hidden ultimatums. Instead, I’m going to recommend alternative thinking about your portfolio here in the Silver Age of the Central Banker.

This is a good example of what I’m talking about. Investment convention holds that you should be fully invested throughout a market cycle. Otherwise you must be—gasp!—a market timer. Boo! Hiss! If there’s a worse insult in the investment world or a quicker way to get fired by your client than to be called a market timer, I’m not aware of it. And god forbid that you actually propose an “alternative strategy” that embraces market timing. But of course, we’re ALL market timers, we just do it in a conventionally acceptable way by “shifting to defensive sectors” or “keeping our powder dry” or “managing risk” (whatever that means). We’re all hypocrites when it comes to our professed faith in full investment, because we don’t really believe in it. We all want to get out of markets when they’re going down, we all want to get into markets when they’re going up, and we all think that we have some insight into what’s next.

And that, of course, is the source of the actual wisdom in this conventional wisdom. We really don’t have a crystal ball to predict whether the market will be up or down tomorrow or over the next week or over the next month or over the next year. We really do have biologically evolved social behaviors that push us to sell low and buy high. Whatever you think you should do as a short-term trade, you’re probably wrong. Left to our own devices, almost all of us are almost always better off to put our investments in a drawer, close our eyes, and walk away.

So here’s the question. How do we change the conversation so that a rigorously conceived adjustment in portfolio exposure to risk assets isn’t characterized as market timing? Because as soon as a strategy is characterized as market timing, then it’s a Hobson’s Choice situation, where you don’t really have a choice but to reject it. Now I’m not talking about reading ZeroHedge and selling because you got all freaked out by an article, and I’m not talking about watching CNBC and buying because you got all bulled up by a talking head. That IS market timing, of an indefensible sort. But is there a defensible sort of portfolio exposure adjustment, one that has a foundation strong enough to allow a non-Hobson’s Choice implementation? My answer: yes. In fact, I think there are two such approaches.

First, markets are more volatile when countries are playing a Competitive game than when they’re playing a Cooperative game. Now granted, this is a prediction of a sort, but it’s a prediction of political dynamics – which is exactly what the game theory toolkit is designed to do – as opposed to a market prediction like whether the S&P 500 will be up or down next week. I think this is where Epsilon Theory can make a unique analytical contribution. The international political regime matters to markets. It matters a lot. I am convinced that we have entered a new, analyzable, competitive regime of domestically stressed nations, and that means that we have a deflationary hurricane brewing. What I don’t know (yet) is whether this is going to be a Category 1 hurricane, a Category 3 hurricane, or a Category 5 hurricane. If China floats the yuan – and that’s the big catalyst I think has a decidedly non-trivial chance of occurring – then it’s Category 5. If they don’t, it’s something less. But regardless, a Competitive global trade game is going to be a big storm. Trim your sails. Whatever that means to you and your investment process, whether it’s increasing cash, reducing net or gross exposure, shifting to long-dated Treasuries … whatever … that’s what I think you should do when the world plays a Competitive game. Does that make me a market timer? Well, if that’s the conversation you’re stuck in … yes. But it’s not the conversation I’m having, either with others or myself.

Second, although I can’t predict future market returns, I can observe how volatile the market has been in the short, medium, and long-term past. It’s that George Soros quote again: I’m not predicting; I’m observing. I can also tell you about my personal appetite for risk and volatility. Put these two items together and you have the foundation for a new conversation about investing, a conversation based on observable risk rather than predicted reward. Is observed volatility going up above a level where I am personally comfortable? Well, let’s take my market exposure down. Is observed volatility going down below that level? Well, let’s take my market exposure up. There are a dozen variations on this theme: call it risk balancing or risk parity or volatility targeting or whatever. But whatever you call it, I think it is a better way of staying invested in markets through thick and thin. Just less invested when thick and more invested when thin.

A systematic risk balancing strategy is at the core of what I have been describing as Adaptive Investing over the past two years. That and an appreciation for the political dynamics that underpin markets, creating different investment regimes as the game-playing moves from one equilibrium state to another. There is zero crystal ball gazing in a risk balancing strategy – zero. In that sense it is entirely compatible with the investment convention of not trying to time markets. But the alternative thinking I’m suggesting here is that “full investment over a market cycle” works better if it’s risk being fully invested over a market cycle, not dollars. It’s a new twist on an old idea, and once you start thinking of risk budgets first and dollar budgets second, everything changes.

I’m pretty sure that I was the first to come up with the phrase “Central Bank Omnipotence.” It was in one of my very first notes – “How Gold Lost Its Luster, How the All-Weather Fund Got Wet, and Other Just-So Stories” – back in the summer of 2013, a note that even today remains one of the most popular in the Epsilon Theory canon. For the next six months or so, however, I would go around and talk with institutional investors about the Narrative of Central Bank Omnipotence – that markets acted as if central bank policy determined market outcomes – and I got enormous pushback. No, no, I heard, we’re on the cusp of a self-sustaining real economic recovery here in the US, and whatever the Fed and other central banks are doing, whatever the market reaction might be, it’s just a bridge to the happy days of “normal” markets ahead. And this is after the Taper Tantrum, mind you. It really wasn’t until the spring of 2014 that the steady drip, drip, drip of the Central Bank Omnipotence meme became a tsunami, and by the fall of 2014 it was impossible to find anyone who didn’t believe in their heart of hearts that Central Banks, for good or for ill, determined market outcomes.

I bring this up because I’ve read lots of suggestions, particularly after the one day half-life of effectiveness for Kuroda’s* negative rates announcement on January 28 and the one hour half-life of effectiveness for Draghi’s negative rates announcement on March 11, that the Narrative of Central Bank Omnipotence is dying. But then you get a day like March 12, where the Narrative engine springs to life in support of Draghi’s “bold move”, and now I read that the Narrative of Central Bank Omnipotence is alive and well.

*Head of the Bank of Japan

Here’s what I think. As the strategic interaction between the four largest economies in the world shifts from self-enforced cooperation to self-enforced competition, from a Golden Age to a Silver Age, so does the market’s Common Knowledge or Narrative regarding that strategic interaction. But it doesn’t die, any more than the strategic interaction dies. Think of it as the same song, but now in a minor key. So long as every CNBC talking head genuflects in the direction of central banks in every single conversation, so long as front page articles about central banks dominate every day’s issue of the Wall Street Journal and Financial Times … then the Narrative of Central Bank Omnipotence is alive and well. The power of the Narrative is that we believe that all market outcomes are somehow the result of central bank policy, not that central bank policy necessarily generates a good or even intended market outcome. It’s a narrative of Omnipotence, not Competence or Omniscience. The day that central bankers give up, the day that Yellen or Draghi appears on stage and says, “Well, there’s really nothing more we can do. It’s just out of our hands now. Sorry ’bout that.” … that’s the day that we lose our religion and the Narrative dies.

Ultimately, we’re no closer to “normal” markets driven by fundamentals here in the Silver Age of the Central Banker – the age of strife and competition – than we were in the Golden Age of the Central Banker – the age of cooperation and great deeds. In fact, we’re farther away than ever. It’s a policy-driven market just as far as the eye can see.

First, we haven’t had a policy-driven market like this since the 1930s, so whatever historical data was used to power whatever model you’re using needs to be taken with a grain of salt.

What this means in practice is that most portfolios are too flabby in what I’ll call the Big Middle – the large portfolio allocation that most investors, large and small, maintain in large cap stocks. The easy way out when it comes to investment conventions and the Hobson’s Choice we all face when it comes to portfolio construction is always to add more S&P 500 exposure. The old IT saying used to be that no one ever got fired for buying IBM, and the current financial advisory saying should be that no one ever got fired for buying more Apple. Although maybe they should.

I’m not saying that capital invested in the Big Middle must always be reallocated to make for a more convex, more diversified portfolio. But I am saying that every bit of your portfolio should be purposeful. I am also saying that there’s a lot of wisdom for investing in what Plato said about politics almost 2,500 years ago (and he was quoting a guy who lived 400 years earlier), that the half is often greater than the whole. Meaning? Meaning that you get better outcomes when half of your citizens or half of your investments are organized efficiently and with right purpose than if all your citizens or all of your investments are organized haphazardly or without common purpose. Or for a more modern slant, I like George Carlin’s take, that while some see a glass half-full and some see a glass half-empty, he sees a glass that’s twice as big as it needs to be. Many portfolios are twice as big as they need to be. Not in dollars, of course (may your portfolio get much larger in that regard), but in terms of inefficient, mushy allocation to low risk, low reward, highly correlated investments.

One exercise I find useful is to think of different future scenarios for the world (not because I’m trying to predict which one will happen, but precisely because I can’t!) and then to consider how my current exposures and strategies are likely to fare in those futures. My goal isn’t to figure out the scenario where I think I’ll do the best, because then I’ll start hoping for it and consciously or unconsciously will start to assign a higher probability of it occurring, but to figure out the scenario where I’ll do the worst (both in absolute terms and relatively to whatever I compare myself to). I’m trying to minimize my maximum regret – minimax regret, a powerful game theoretic tool for dealing with technical uncertainty, where you’re not sure that you’ve identified all the potential outcomes and you’re certainly not sure of the probability distribution to assign to those outcomes – and I do so by planting seeds (buying exposure with either embedded or overt optionality) in that least happy scenario. I find that this iterative, new information-friendly exercise changes the conversation you can have with others or yourself, away from a needlessly daunting conversation on risk/reward maximization and towards a more fruitful conversation on being an investment survivor in a decidedly dangerous time.

And now for the big finish.

Last summer I wrote a note called “The New TVA”, which made a direct comparison between the political dynamics of the 1930s and the political dynamics of today. What amazes me (still), is how the political conversations then are almost identical to the political conversations now.

Just switch out FDR for Obama and you could easily imagine this cartoon being about healthcare or some such rather than New Deal legislation.

Here’s the skinny for that note: in the same way that FDR had an existential political interest in generating inflation and preventing volatility in the US labor market, so does the US Executive branch today (regardless of what party holds the office) have an existential political interest in generating inflation and preventing volatility in the US capital markets. Transforming Wall Street into a political utility was an afterthought for FDR, a nice-to-have but not a must-have, as Wall Street was not yet a Main Street phenomenon. Today the relative importance of the labor markets and capital markets have completely switched positions. Wall Street is now decidedly a Main Street phenomenon, and every status quo politician – again, regardless of party, and let’s remember that the Fed is part of the Executive Branch – keenly desires to keep the genie of unfettered fear and greed firmly stopped up in its bottle. Georges Clemenceau, French Prime Minister before and after World War I, famously said that “war is too important to be left to the generals.” Today, the quote would be “markets are too important to be left to investors.”

But it was only after Draghi’s ECB announcement on March 10th that I think I see how a policy-driven market becomes a policy-controlled market. The ECB took a page from the Bank of Japan’s (BOJ) playbook and announced that they would now buy non-bank investment grade corporate credit as part of their QE asset purchases, and that’s at least as big of a deal as the BOJ taking a page from the ECB playbook in January and adopting negative interest rates. When two of the Big 4 adopt any policy, a point becomes a line and an idiosyncrasy becomes a pattern. The direct purchase of corporate securities by central banks is now in the official tool kit of every central bank. You cannot un-ring this bell. It is a “Goodfellas moment” of enormous consequence.

In one fell swoop, Draghi has essentially made useless the most effective portfolio hedge I know against systemic risk – shorting investment grade credit through the CDS* market. And he conceived this plan when senior bank debt CDS spreads (the best indicator of systemic risk levels I know) were only 120 bps wide! Imagine what’s going to happen the next time spreads blow out to 200 bps wide, much less if we ever got close to the 350 bps spread of 2011. My point, of course, is that Draghi isn’t going to allow CDS spreads to blow out again. Ever. Not even a little bit. The ECB will intervene directly in credit spreads from here to eternity, first in sovereign debt, now in non-bank corporate debt, tomorrow in bank corporate debt. That’s how a policy-driven market becomes a policy-controlled market, not by outlawing short sales or credit default swaps, but by sitting down at the poker table with an infinitely large stack of chips relative to any other player. The ECB can now run over anyone who sits down at the European corporate credit poker table. Thanks, but I’d rather not play, no matter what cards I’m dealt.

*CDS stands fir Credit Default Swaps. The prices of these equate to credit spreads and represent the rick that a bond will default.

But, Ben, what about stock picking? Yeah, what about stock picking? You can read the S&P scorecard here. How did that actively managed US equity fund work out for you last year? Or the last 5 years? Or the last 10 years? Here’s my issue with stock picking. Most stock pickers look at companies pretty much exclusively through the lens of “quality” – a quality management team, a quality earnings profile, a fortress balance sheet, etc. Unfortunately, this is the worst possible investment perspective to use in a policy-driven market, much less a policy-controlled market. It does not outperform a broad passive index. It does not generate alpha. Again with the George Soros quote: I’m not expecting it; I’m observing it. I know, I know. Heresy. But ask yourself this. Do you really think that the mandarins of the Fed or the ECB or the BOJ care one whit about whether this company or that company has a higher stock price? Of course not. They want ALL companies to have a higher stock price, and as a result the policies they are going to implement will inevitably help the weakest, lowest quality companies the most. Now if investing in quality-uber-alles is the conventional conversation you need to have to justify participating in public markets, I get it. But to me it’s just another form of fighting the Fed, and for me it’s always a losing conversation.

So if I can’t protect my portfolio through effective shorts, and the Powers That Be are determined to turn public markets into political utilities, but I’m structurally bearish on the ability of the Powers That Be to prevent domestic political shocks and international political conflict of 1930-ish proportions, what’s to be done with public market investing other than the occasional short-term trade? Two things, I think.

First, I think it makes sense to use public markets for their liquidity and for tapping whatever this utility-like rate of return the Powers That Be have in mind. But I also think it makes sense to tap global beta through risk balancing strategies, because I really do think we’re in for a bad storm, and I don’t trust Captain Yellen or Captain Draghi to guide the ship for my benefit rather than their own political benefit. As for any effort to find alpha in public markets? Forget it.

Second, I think it makes sense to use public markets if that’s the best way to own real assets. Why real assets? Because while nothing is immune to the predation of illiberal governments and the capricious rule-making and rule-breaking of central banks, real assets are at least insulated from both. What real assets? I have a very broad definition, including not only the obvious suspects like real estate and infrastructure and commodities, but also gold and intellectual/digital property. Actually, I think of gold as very similar to many forms of intellectual property, as its worth is found in behavioral preferences and affect, not in some intrinsic or commercial use case.

All real assets are not created equal, of course. I’d much rather own an asset that generates some sort of cash flow than one that just sits there, but price will usually (although not always) take care of that differentiation. The most important consideration, I think, particularly when using public markets, is to get as close as you can to the fractional ownership share in the asset itself and as far away as you can from the casino chip. What that means in practice is getting as high up in the capital stack as you can while still having an equity claim on assets. For a highly levered or distressed company that probably means being in the senior secured debt. For a more typical company that might mean being in the preferred equity shares, if they exist, or choosing between this company’s equity and that company’s equity. It’s making this sort of evaluation where I think that active managers, whether it’s in equity or in fixed income, can prove themselves, and where I think there’s a role for fundamentally-oriented, stock-picking active managers. It’s not because I think they can stock pick their way to outperformance versus a passive index while we’re in a policy-driven or policy-controlled market, but because I think they can identify a margin of safety in my public market ownership of real assets and real cash flows better than a passive index. Now that’s a conversation worth having with active managers here in the Silver Age of the Central Banker.

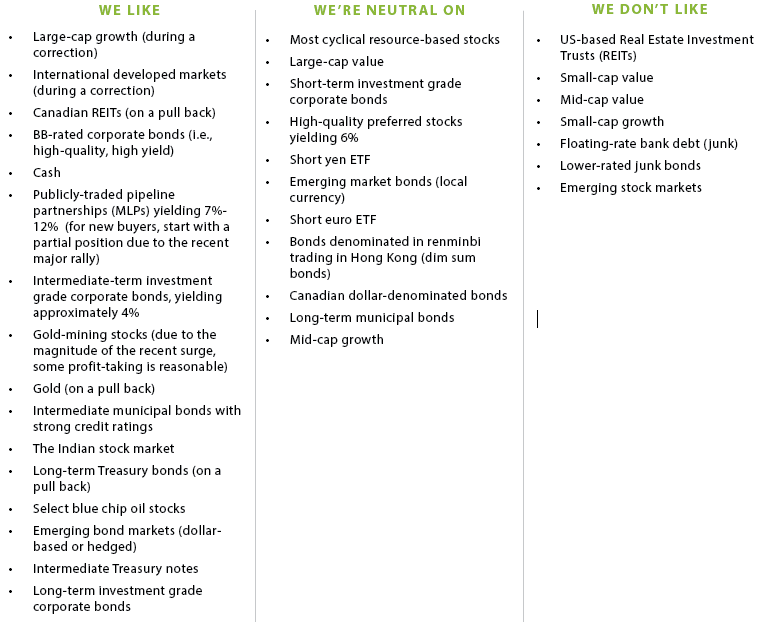

OUR LIKES/DISLIKES

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.