“Future economic historians will look back at the first quarter of 2016 as the turning point; that was the end of the hangover induced by the global financial crisis.”

-NIALL FERGUSON

Is it possible? Could it be true? Might Brexit actually be bullish for financial markets? Few would have dreamed this possible a week ago but one of those rare individuals was—and still is—Vincent Deluard, among the keenest minds at Ned Davis Research. Vincent’s thesis is that the chaos created by Brexit gives the world’s central bankers a green light to yet further saturate the world with their make-believe money, once again bailing out financial markets. He actually goes so far as to muse about the possibility of a “melt-up” in stocks, caused by another torrential downpour of manna from central bank heaven.

Ironically, his suggestions in a series of emails to me this week are consistent with the first half of the EVA we were planning to send out last Friday. But, as noted at the time, the British vote caused the Evergreen Gavekal team to rapidly shift gears and focus on that shocking event. Now it’s time to run our delayed Guest EVA which contains an attitude shift that is almost as surprising as Brexit.

EVA readers are likely to have vivid memories of this month’s Guest edition author, Worth Wray. Worth wrote a number of EVAs in the second half of 2015 and earlier this year before returning to his Texas roots a few months ago, becoming the Chief Economist for STA Wealth Management in Houston.

Worth and I have maintained contact since his friendly departure and he was kind enough to add me to the distribution list for his weekly newsletter titled, appropriately enough, For What It’s Worth. He also attended the recent Mauldin Strategic Investment Conference (SIC) in Dallas, as did several Evergreen team members. (If you missed our overviews of the SIC, published a few weeks ago, you can read them here: part one and part two). Worth was particularly intrigued by the comments of acclaimed economist and historian Niall Ferguson, one of the keynote speakers at the SIC (but who I missed, unfortunately).

Veteran EVA readers may recall my focus on Professor Ferguson’s presentation at the SIC a few years ago in which he discussed the thesis of his then new book, “The Great Degeneration”. As the title implies, it was a scathing critique of current developed-world policies, particularly what he pithily referred to as “The Rule of Lawyers”. This was meant to be a play on the sacrosanct notion that the “Rule of Law” is essential for healthy economic development. Professor Ferguson’s thesis, until recently, was that it was being perverted by many in the legal profession (aided and abetted by the political class, who also frequently are, or were, attorneys).

Accordingly, as Worth points out, when someone like Prof. Ferguson does a complete about-face—shifting, as he has done, from the catcalling-to the cheering-section of the bleachers—it’s a highly noteworthy development. Because one of the goals of EVA is to examine both the bull and bear case, we were particularly inclined to share this “epiphany” with our readers. Without giving away too much about his position shift, suffice to say that, like Vincent, he believes central banks have won the battle against the forces of stagnation and government paralysis (though the latter believes they may very well lose the war).

As mentioned above, Worth is presenting both sides of The Great Debate on whether current policies are working or failing, by also including a counterpoint section focused on hedge fund icon John Burbank. As you will read, Mr. Burbank has a much darker view of current conditions (including a 66% chance of a US recession soon). While Evergreen continues to lean toward the latter viewpoint, we will once again emphasize that since no one has ever seen this set of financial and economic circumstances before—made even more unparalleled by Brexit—keeping an open mind is essential. As the old saw goes, a mind is like a parachute—it only works when it is open.

David Hay

By Worth Wray

-This week’s issue of For What It’s Worth features two of the world’s sharpest macro thinkers: Niall Ferguson & John Burbank.

-Though they both believe – as I’ve been writing since mid-March – that global policy elites are working behind the scenes to stave off a global financial crisis and stabilize global markets, Niall believes this effort is working and John believes it’s bound to fail.

-That simple disagreement leads them to dramatically different macro outlooks.

-At STA Wealth Management, we are positioning our client portfolios to manage the downside risks that Burbank describes while staying alert to any meaningful signs that Ferguson’s “inflection point” thesis rings true over time.

-While Niall Ferguson believes historians will look back on February 2016 as the inflection point where the world started to work off its post-2008 hangover, John Burbank believes the temporary reflation we’re seeing in global markets may eventually give way to a global liquidation event compounded by the risk of a US recession, a Chinese RMB devaluation, and a Trump US presidential win.

-In the end, there can be only one; but we’ll only know for sure with the benefit of hindsight.

This week’s issue of For What It’s Worth features two of the sharpest macro thinkers in the world: Niall Ferguson & John Burbank.

Though they agree – as I’ve been writing since mid-March (see “Did Central Banks Just Save the World,” & “You Can’t Blame Them for Trying”) – that global policy elites are working behind the scenes to stave off a global financial crisis and stabilize global markets, Niall believes this effort is working and John believes it’s bound to fail. That simple disagreement leads them to radically different outlooks. And like Sean Connery’s character notes in the 1985 classic The Highlander, “In the end, there can be only one.”

Aside from his current role as a Senior Fellow at Stanford University’s Hoover Institute, Niall Ferguson is one of the world’s leading historians, a recently retired Harvard University professor, and the author of fourteen books including The Ascent of Money, Civilization, Empire, Colossus, The Great Degeneration, and The House of Rothschild.

He has also been a rather outspoken critic of the warped, model-driven thinking that’s captured the world’s most influential policymaking institutions like the Federal Reserve, the European Central Bank, or the International Monetary Fund in recent years… which makes his most recent comments so interesting.

All of the sudden, Professor Ferguson has changed his tune.

Central banks – he now argues – are winning the war against deflation. Not only did they prevent a replay of the Great Depression in 2008 and 2009, and save the Euro Area from outright collapse in 2012, but now they’ve managed to set the global economy on a radically new path in February 2016.

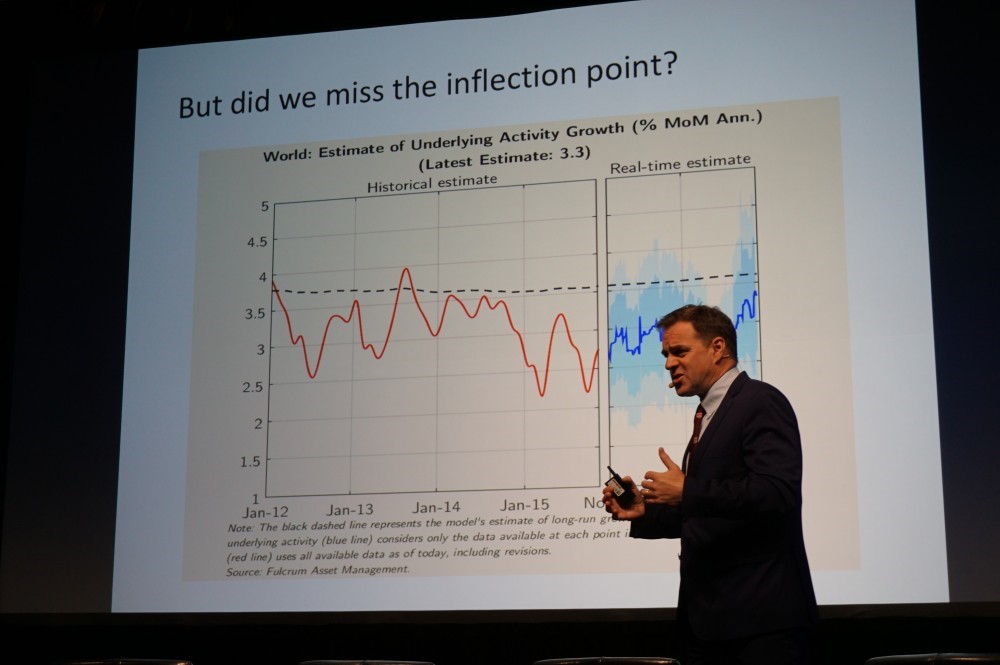

Most people are still missing it, as he explained to a packed house at John Mauldin’s latest Strategic Investor Conference, but that’s the nature of turning points.

“The inflection point is happening,” he said in an interview with the Financial Review shortly before Mr. Mauldin’s Strategic Investor Conference. “But it will only be visible in about a year, and is barely perceptible to most people now… but there are forces that are turning the world economy around.”

On this point, let me just say that I understand where Niall is coming from (for at least part of his argument)… and I am baffled by his overwhelming sense of certainty. [To be clear, I’m not trying to criticize or belittle the Professor’s view. This is one of the most interesting macro arguments I’ve heard in months and I DESPERATELY want to know why he feels so certain that February 2016 was the inflection point in our global debt, demographic, & deflation drama.]

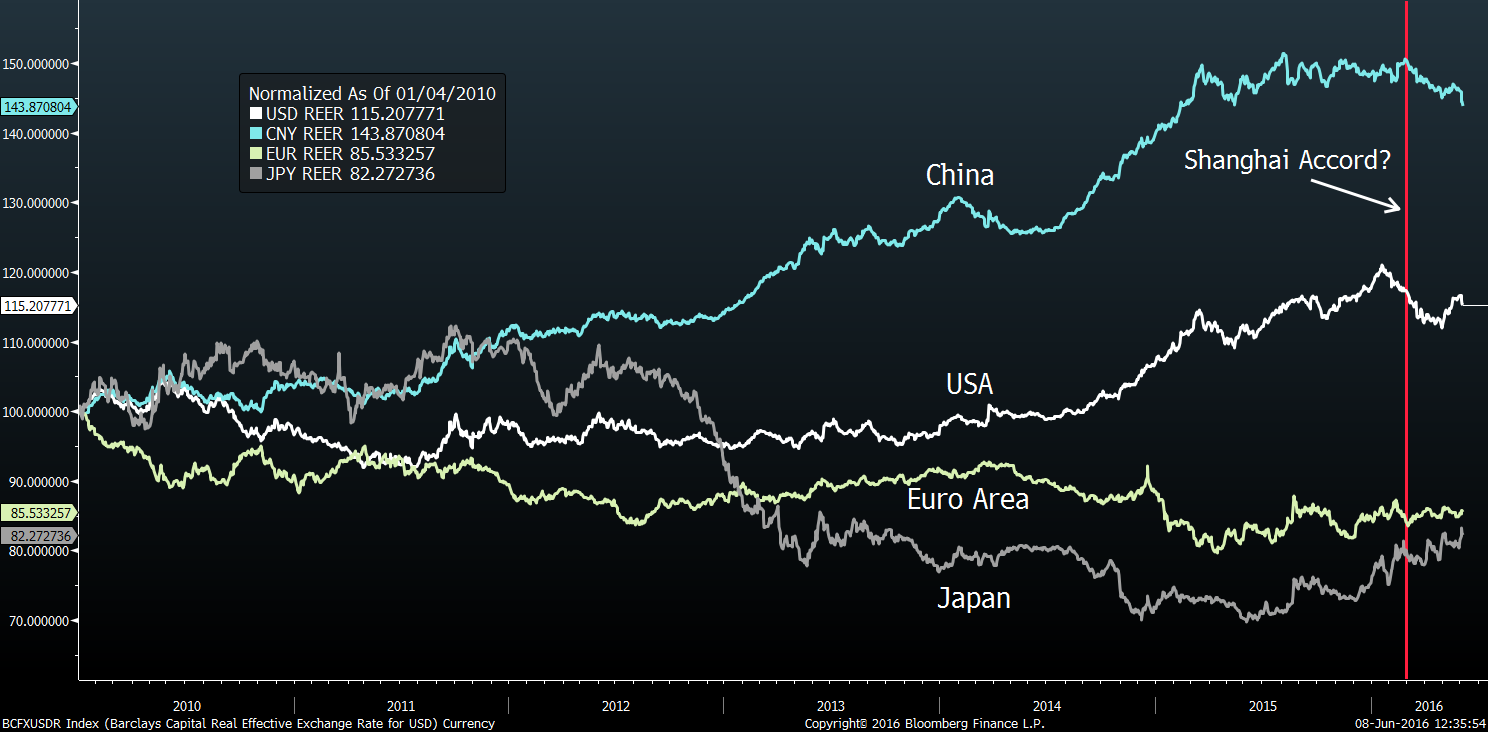

If you recall, I offered a similar hypothesis in mid-March when – immediately after a quiet meeting on the sidelines of the G-20 summit in Shanghai – the European Central Bank, the Bank of Japan, and the Federal Reserve all appeared to prioritize weakening and containing the US dollar over their domestic policy goals (“Did Central Banks Just Save the World?”).

While Japan and Europe had been winning the currency wars by steadily weakening their exchange rates against the United States and China, this kind of “every central bank for itself” policymaking brought the world to the edge of a global crisis by early 2016.

Source: Bloomberg

Source: Bloomberg

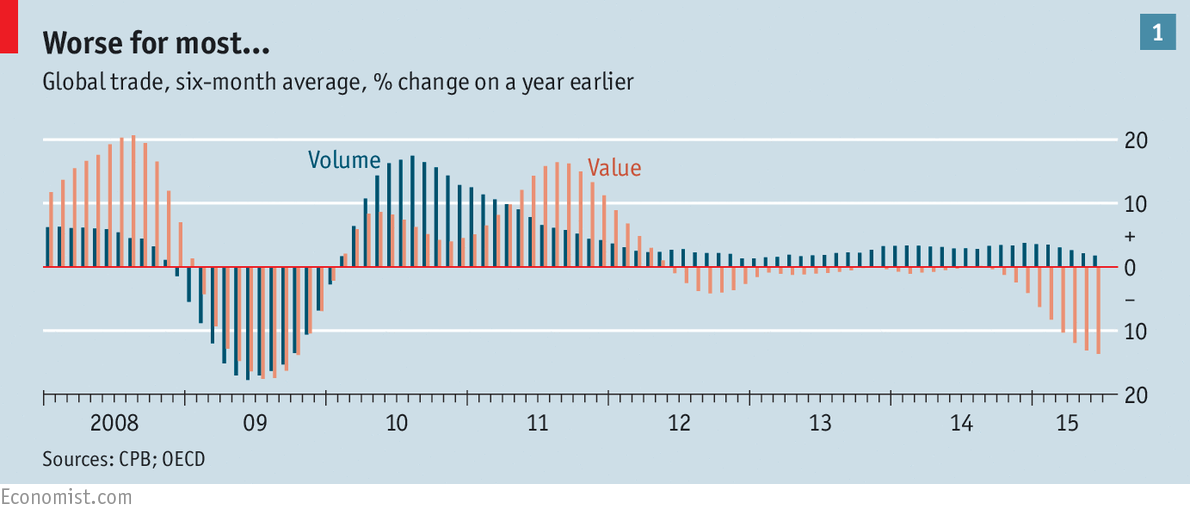

Not only did the divergence* between foreign central banks and Fed policy result in a big rise in the US dollar, it also led to a disorderly drop in the price of dollar-denominated commodity prices, an outright exodus of foreign capital from major emerging markets like China, Russia, Brazil, and South Africa, and a 15% collapse in global trade in US dollar-terms.

Needless to say, these trends created waves in global economic and financial systems still trying to heal from the 2008 downturn and threatened to unleash enormous shocks unless global policy elites opted to intervene by weakening/containing the US dollar and stemming the tide of outgoing capital from the People’s Republic of China. I did not think such an arrangement was possible in the run-up to the G-20’s late February gathering of central bankers and finance ministers in Shanghai, but that’s exactly what we started to see in mid-March.

First the European Central Bank cut its target interest rate and expanded its asset purchase program to include corporate bonds while Mario Draghi intentionally reset the market’s expectations for future easing. Rather than falling on new stimulus, the euro rallied.

Source: Bloomberg

Source: Bloomberg

Then Bank of Japan Governor Haruhiko Kuroda backed off on his February guidance to keep dropping his target interest rate deeper into negative territory and proceeded to sit on its hands for the following three months. Like we saw in Europe, the Bank of Japan allowed the yen to rise despite its domestic policy needs.

And finally, the Federal Reserve dropped its 2016 guidance from four rate hikes to two before Janet Yellen delivered one of the single most dovish speeches in recent memory citing concerns that the disorderly drop in oil prices along with uncertainty surrounding China’s exchange rate called for extreme patience in hiking US interest rates

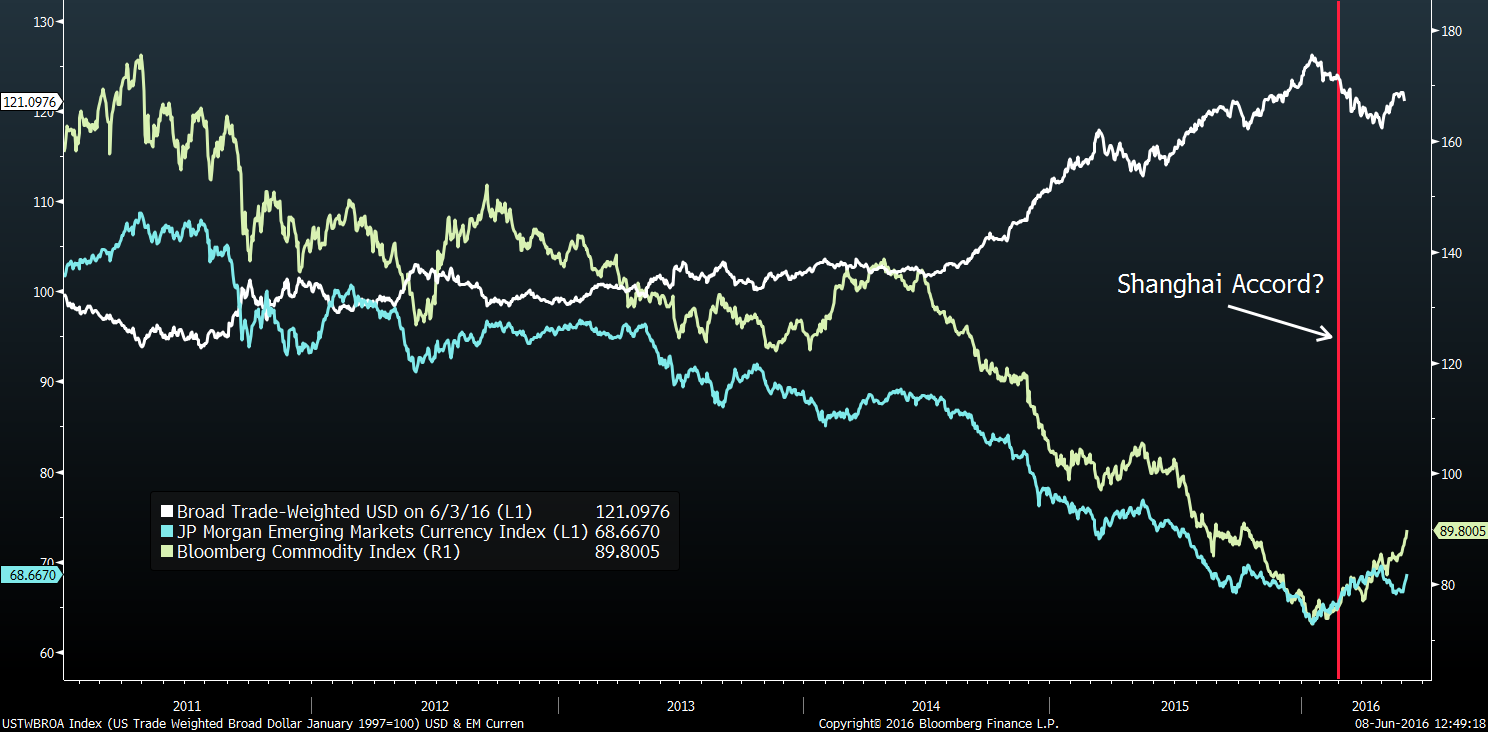

As you can see in the chart on the next page, these collective moves led to a big drop in the US dollar, a resurgence in global commodity prices, and a modest reflation in emerging market currencies…

Source: Bloomberg

Source: Bloomberg

… along with a distinct weakening in China’s exchange rate versus its other trading partners while holding steady with the US dollar.

Incredible, right?

After catching hell for this thesis over the last few months, I was surprised and pleased to hear an eminent macro thinker and A-list policy insider like Niall Ferguson (the Niall Ferguson) acknowledge and agree with an idea as controversial as the “Shanghai Accord.”

In fact, he called it “the most interesting question of the year” and said “this is why the inflection point is so plausibly now.”

Still, I was surprised to see him take such an aggressive view. Ferguson is not just risking his reputation with such a bold a macro call, he’s also risking his business.

What you may not know about Niall is that he quietly works with a small group of elite hedge fund managers and corporate executives as the Managing Director of a macroeconomic and geopolitical advisory firm called Greenmantle. He may not manage money directly, but the Professor advises on a major pool of assets and a global network of businesses.

Something clearly happened in Shanghai, but – as I’ve chronicled for the past several months – there’s a big difference between a tacit central bank ceasefire and a coordinated effort to boost global growth.

Much to IMF** Managing Director Christine Lagarde’s dismay, we still aren’t seeing the advanced economies – aside from China and maybe Japan – taking decisive action to build on this fragile ceasefire in the currency war and secure more durable global growth with government-led infrastructure investment and/or growth-unlocking structural reforms. And we’re still not seeing any meaningful progress toward the kind of international monetary reform that would make the world less vulnerable to swings in the trade weighted US dollar.

In the absence of such moves, I can’t – for the life of me – see how the Shanghai Accord can hold together until 2017, much less mark a global turning point. But perhaps Mr. Ferguson knows something I don’t. I have to admit it’s a distinct possibility given his access to global elites and the time he spent this past April with Ms. Lagarde.

Then again – as the rest of Professor Ferguson’s presentation suggests – we may just see the world unfolding in different ways.

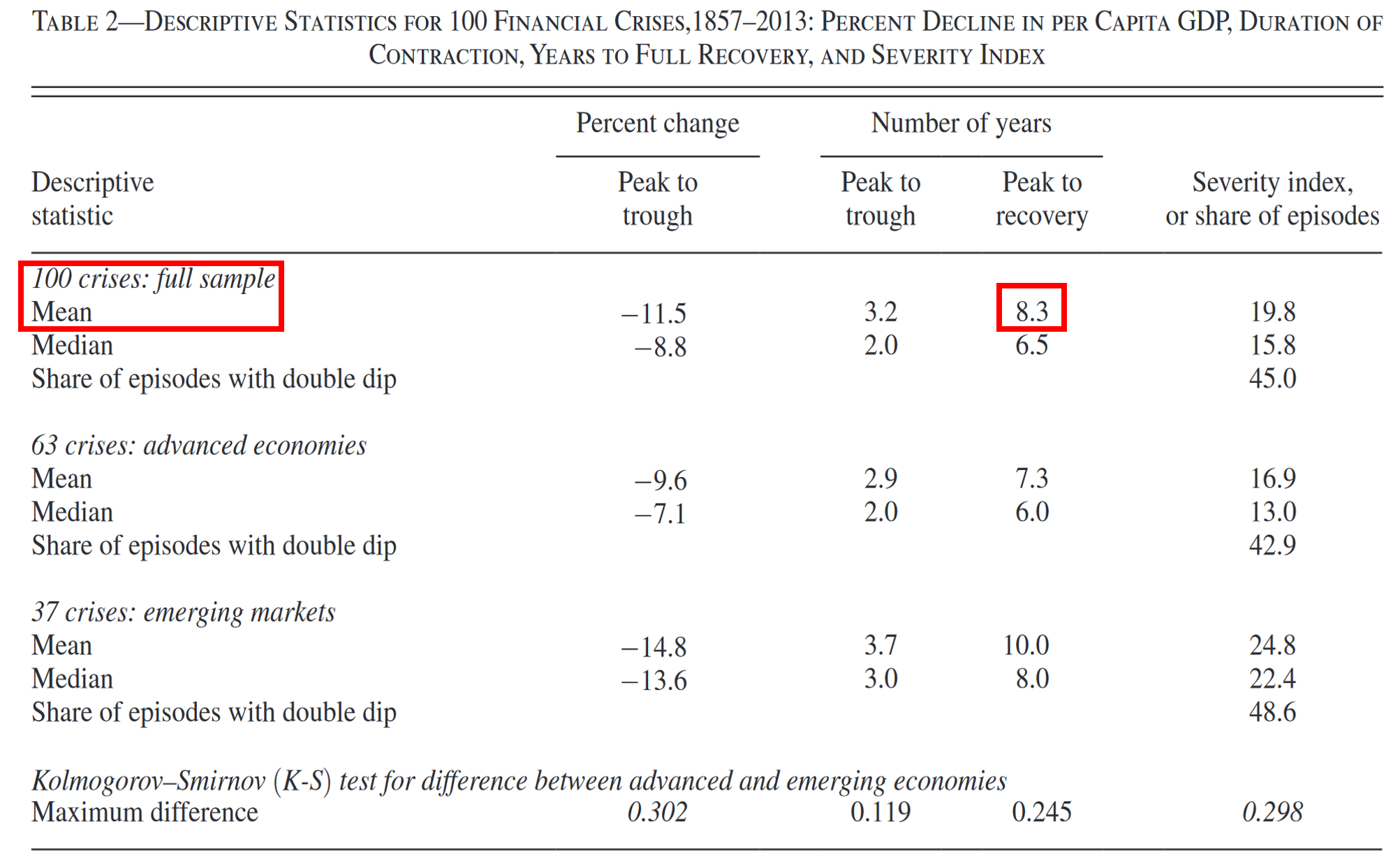

While Niall admits this theory may turn out to be wrong, he believes the global economy is slowly recovering from its post-2008 hangover like Carmen Reinhart and Kenneth Rogoff told us to expect in their exhaustive study on financial crises, This Time is Different.

As you can see in the chart below (taken from Reinhart & Rogoff’s 2014 paper, “Recovery from Financial Crises: Evidence from 100 Episodes”), the average recovery time after major financial crises tallies to roughly eight years.

Ferguson argues that puts us right on time, for the hangover to wear off, for global growth to re-accelerate, and for former US Treasury Secretary Larry Summers’ “secular stagnation” theory to fall flat. Instead of stagnating for the foreseeable future, Niall believes the US, China, and much of Europe are in the process of picking up steam.

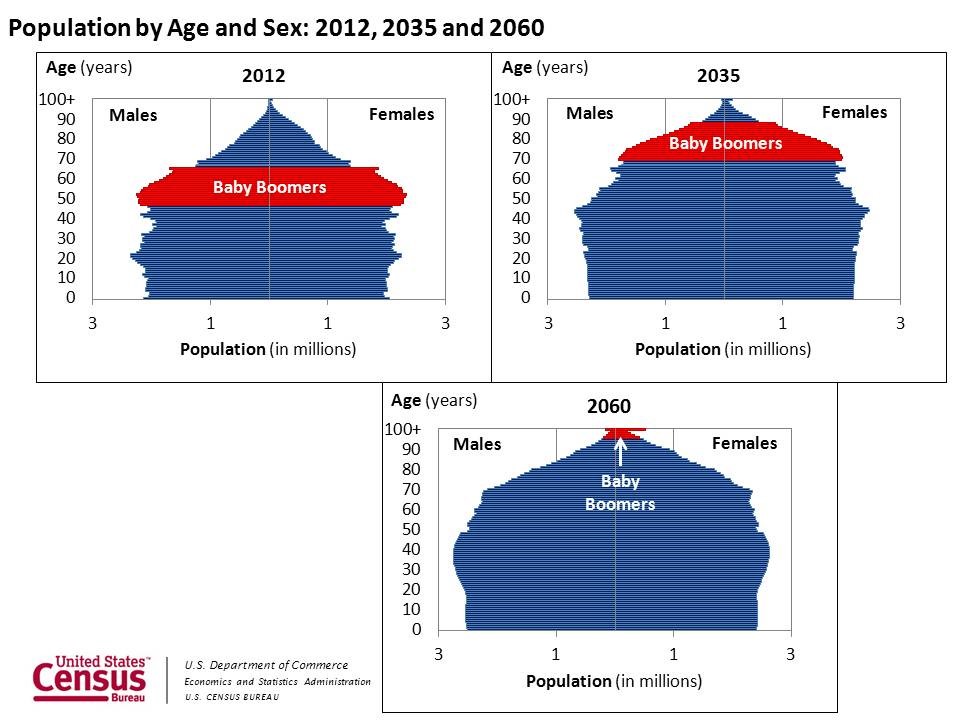

What’s more, he believes the US demographic bulge is starting to pass as retiring Baby Boomers set the stage for a tightening labor market.

That’s certainly a variant perception. And while he admits a number of tail risks like the rise of Trump-style populism and trade protectionism, premature Fed rate hikes, or a shift away from Chinese economic reforms could threaten his outlook, Niall Ferguson is more optimistic than I’ve seen him in years.

The question is, is he correct? Remember, there can be only one.

As the Founder and Chief Investment officer of Passport Capital, John Burbank manages roughly $4.1B across three hedge fund strategies and has been recognized by Barron’s and Absolute Return magazine for running one of the world’s top performing hedge funds.

Not only was he one of the few investors to see the global financial crisis coming far enough in advance to make a fortune betting against subprime mortgages in 2007, but he was also one of the few investors to see the recent breakdown in global liquidity and commodity prices as global policy divergence fueled the US dollar higher and drove China’s RMB to a breaking point in late 2015 and early 2016.

In short, Burbank is a global macro legend… and, as Bloomberg’s Saijel Kishan reports, he’s not convinced the recent weakening in the US dollar or rebound in global financial markets signals a fundamental shift.

Instead, his outlook sounds a lot like our STA Investment Committee view that the world is simply working its way through the eye of the storm.

“This is a time full of peril and repositioning,” he wrote in a recent letter to investors. “[It] heralds either the start of a new market reality (i.e. inflation and too much liquidity) or the beginning of the liquidation.”

I don’t know if Burbank specifically believes in the Shanghai Accord, but he’s made it exceedingly clear that major central banks have become “very proactive” since February.

“They’re trying to exert control to prevent bad things from happening,” he told Wall Street Week’s Anthony Scaramucci and Anthony Kaminsky. “I thought there was going to be a deflationary collapse at the beginning of the year; and in some respects – maybe for the wrong reasons – the Fed flip-flopped at a time that rescued the markets temporarily.”

There’s the key one-word difference between Ferguson and Burbank: “temporarily.”

While Niall sees the collective efforts of major central banks as the turning point for a global recovery, John describes it as little more than a pause.

“Last year we thought the end of QE at the end of 2014 would lead to a stronger dollar… The Fed’s move to be dovish for a few months has hurt the dollar. I think the dollar is bottoming and I think it’s going to resume its ascendance, which is going to hurt liquidity in a lot of things like [emerging markets] and commodities.”

If you read my note in month’s STA Market Report, then you know that fluctuations in the trade-weighted US dollar has both direct and indirect effects on global liquidity. In direct terms, the US dollar is the world’s dominant funding currency. In other words, foreigners tend to borrow in dollars when dollars are cheap, and they tend to get squeezed – sometimes to the point of default – when dollars get more expensive.

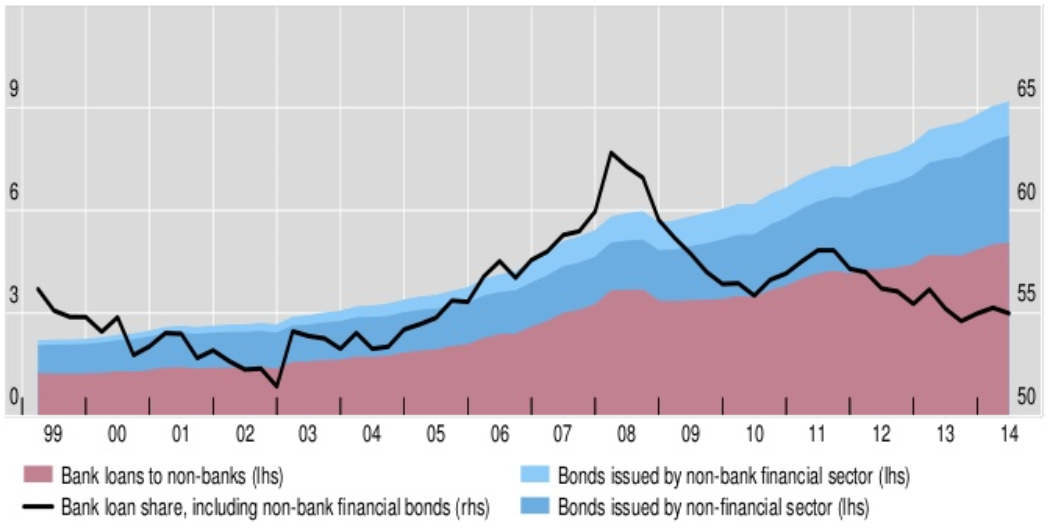

Cross-border Credit Denominated in US Dollars

(Outstanding Stock in Trillions of Dollars--Left Scale--versus Percent in Bank Loans--Right Scale) Source: The Bank for International Settlements

Source: The Bank for International Settlements

In addition to subjecting emerging market borrowers to painful boom-and-bust cycles over the last several decades, this dynamic has resulted in a serious build-up of cross-border dollar-denominated debt totaling more than $9 trillion (and potentially more than $10 trillion since this chart from the Bank for International Settlements was last updated in early 2015) on top of a total global debt burden now exceeding $200 trillion.

But along with weaker commodity prices, that’s just the first-order impact of a rising dollar.

In indirect terms, the greenback’s influence is even more powerful. Since a stronger US dollar and higher nominal US interest rates tend to trigger capital flight out of vulnerable markets, foreign central banks are often forced to hike their domestic interest rates even in the face of weakening economies to resist sharp collapses in their currencies. As a result, global liquidity tends to dry up when the US dollar rises, especially when the Fed is hiking rates.

That’s the environment Burbank expects when the US dollar breaks out again in the coming months. He says it could trigger a global “washout” where global liquidity dries up and asset prices tumble.

Moreover, he sees three risks that could usher in such an event.

First, the US could fall into recession, which he handicaps at a roughly 66% probability. “I think [the odds of recession] are very high. It’s remarkable how little people regard this risk.”

Second, China could devalue the RMB. “They have to recap their banks. [Non-performing loans] are huge. The question is when do they do it? I think they’re waiting until after the US election.”

Third, Donald Trump could win the US Presidential election. “It’s feared by foreigners more than actual Americans… I actually don’t [fear a Trump presidency], but I think the discounting of a potential Trump win [i.e. a market sell-off in the event the brash New Yorker does win] is something you need to hedge yourself against.”

Personally, I don’t see these as “tail risks.” I see them as dominant probabilities – along with potential shocks from surprise easing in Japan or even a Brexit when UK voters take to the polls on June 23 – as 2016 slowly gives way to 2017.

If you want to look for a silver lining, the good news is that Burbank’s US recession and global liquidation scenario could eventually lead to another major turning point for the US economy where the US government embarks on an ambitious infrastructure investment program.

“If that actually happened,” Burbank says, “it would be good for US growth. But it would be very domestic growth focused, so we’d want to be longer US equities and shorter the rest of the world. The issue is what level will the dollar be? And will the Fed participate in such a way to lower the dollar or not. That would determine how long I’d be the US market.”

Finally, the hedge fund manager describes his ideal scenario based on Passport’s current portfolio positioning.

“The dream set up for me in the hedge fund is that we do get a US recession, we do get a China deval, Trump is elected, there’s a washout of liquidity… and then in 2017, after this recession is widely understood, there is a big infrastructure program. The Fed realizes it’s too tight with monetary policy, it does something to relieve the dollar, and then asset prices do very well in the United States.”

As I’ve experienced a handful of times in my career, world class global macro thinking often feels like reading the newspaper six months in advance.

Both of these guys have that gift. They do their homework, trust their intuition, and stick their necks out on ideas most people consider crazy at the time… even at the risk of being completely wrong as the story unfolds.

Like the brilliant investment writer Jim Grant always says, “Successful investing is about having everyone agree with you… later.”

The question is, who will we all agree with in eighteen months as we look back on 2016 and 2017 with the benefit of 20/20 hindsight?

I have to admit, my money’s on John Burbank. We have a similar framework for thinking about global markets and I think he appreciates how fragile our messy dollar-based system has become.

While I’d like to agree with Niall Ferguson, I still see a world drowning in debt, distorted by demographics, and disrupted by rapid technological advances… not to mention 1930s-style nationalism and protectionism in the US, Europe, and Asia.

In some ways, history can be extremely informative. In other ways, we’re working through a global shift that has never happened before.

While our two “immortals” stick their necks out, my colleagues and I on the STA Investment Committee are charged with a different mandate than posting huge returns at the risk of major losses. We’re focused on guiding our clients through the storm with enough capital to take advantage of whatever opportunities the next cycle presents.

In the event that Professor Ferguson is right, we can pivot our client portfolios back toward higher-risk global assets with a focus on low valuations and favorable macro trends; but if Mr. Burbank is right, our clients can sleep well at night knowing that we are carefully managing that downside risk.

-Worth Wray, Chief Economist & Global Macro Strategist, STA Wealth Management

*Note: Easing by overseas central banks vs. the Fed tightening

**Internatonal Monetary Fund

OUR LIKES AND DISLIKES

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.